LPG, Shale Oil, and New Market Opportunities for High-Value Blendstocks

Shale oil and gas operations in North America generate abundant and low-cost supplies of LPG. At the same time, high production levels of shale oil and gas have created new niche market opportunities for high-octane gasoline and low-temperature diesel blendstocks.

For decades, the industry has explored combinations of technologies capable of converting LPG components—propane and butane—into gasoline and diesel blendstocks. However, before the emergence of significant pricing differentials between oil, gas and LPG, these approaches were not economically viable.

Today, with new process intensification methods, more efficient separations, and advances in dehydrogenation and olefin conversion technologies, the economics have shifted. North American LPG can now be converted into high-value, high-volume products that meet growing market demand.

Opportunity in Lower Hydrocarbons

Low-cost natural gas, ethane and propane extracted from shale operations represent major opportunities for the U.S. petrochemical sector. Prior to the 2014–2015 oil price collapse, U.S. petrochemical margins were exceptionally strong. Abundant “wet gas” production kept NGL prices low, enabling ethane and LPG to replace costly naphtha as feedstock in ethylene crackers.

U.S. ethylene and derivatives—produced from this advantaged NGL feedstock—competed globally against naphtha-based production, benefiting from attractive spreads.

After the 2014/2015 oil price decline, naphtha prices fell sharply, compressing margins. Yet this also pushed NGL prices down further, as shale producers continued high output rates to maintain cashflow.

Emerging LPG Monetization Projects

Several significant LPG-related projects have emerged:

- Ethane export projects supplying Europe and the Middle East

- Growing U.S. LPG export volumes

- Propane dehydrogenation (PDH) units for polymer-grade propylene

- Power generation using ethane

However, each of these markets is constrained—either by limited capacity, logistics, or modest long-term demand growth.

Refinery Fuel Gas Upgrading

In refineries, propane and butanes—often mixed with olefins—are typically burned as low-value fuel gas. With low U.S. natural gas prices, this represents a significant undervaluation.

Upgrading these refinery offgases presents another attractive opportunity, especially when leveraging:

- Existing utilities

- Lower brownfield capital costs

- On-site dehydrogenation and olefin conversion technologies

Market Niches Created by Shale Oil

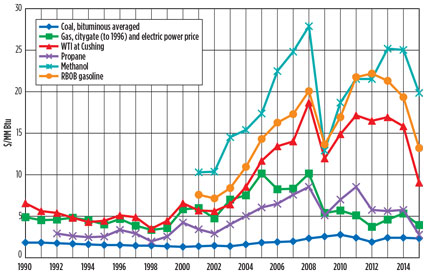

Shale oil is lighter and more paraffinic than heavier imported crudes. As a result, it produces fewer high-octane aromatic compounds, creating a deficit in premium gasoline blendstocks.

At the same time, petrochemical crackers shifting to ethane and LPG reduced the availability of butylenes for alkylation, further tightening global octane supply. This imbalance has elevated prices for high-octane components such as MTBE.

Diesel and jet fuel markets also continue to grow faster than gasoline, with shortages recorded in Europe, the U.S. Midwest, West Africa, and India.

Enabling Technologies

Converting propane or butane into high-value products typically involves:

- Dehydrogenation to form olefins

- Oligomerization to produce higher hydrocarbons

- Cyclization and aromatization pathways enabled by zeolite catalysts

These olefin conversion technologies are essential in producing:

- High-octane gasoline blendstocks

- Low-temperature diesel or jet blendstocks

- Chemical intermediates (C5–C14)

- Industrial lubricant basestocks

Historically, high capital and operating costs limited deployment, but new intensified and integrated process designs have dramatically improved cost-efficiency.

Integrated Processes for LPG Conversion

New process configurations integrate dehydrogenation, olefin concentration and olefin conversion steps using clever distillation-side reactors. These hybrid systems:

- Reduce expensive cryogenic separations

- Improve heat integration

- Achieve high conversion with lower energy input

- Enable scalable production of high-value blendstocks

Depending on catalyst and reaction pathways, outputs may include:

- Cycloparaffins

- Alkylaromatics

- Diesel-range oligomers

- Lubricant-range molecules

Takeaway

North America's abundance of low-cost propane and butane creates a powerful opportunity for the development of new, high-value markets. Technologies that once lacked sufficient economic justification are now attractive due to:

- Improved process intensification

- Greater LPG surpluses

- Global octane and diesel shortages

- Growing petrochemical demand

By integrating olefin generation and olefin conversion technologies—while simplifying separations through advanced process design—the industry can unlock profitable new outlets for oversupplied North American LPG.

About the Author

With extensive experience in international finance, the author structures high-level funding

solutions for governments, private corporations, public–private partnerships (PPP),

and large-scale development projects across energy, infrastructure, real estate,

education, healthcare, agriculture, and humanitarian sectors.

Operating through a global network of top-tier banks, institutional partners,

private capital groups, and regulated financial platforms, the author manages

confidential and compliant strategies involving SBLC, BG, MTN, DLC,

trade finance, structured finance, and monetization frameworks.

All processes follow strict AML/KYC, due diligence, and international regulatory

standards.

The author’s mission is to simplify access to world-class financial knowledge and

bring clarity to complex funding mechanisms, empowering governments, communities,

and project owners to realize transformative initiatives that enhance education,

healthcare, housing, clean energy, and economic development in emerging regions.

Professional Engagement & Confidentiality

All interactions are confidential, conducted with integrity, and aligned with

international compliance protocols.

No public fundraising, investments, or financial solicitations are offered.

Each project is treated with discretion, professionalism, and strategic precision.

Important Legal Disclaimer

This content is strictly educational and informational.

It does not constitute financial advice, investment solicitation, securities

promotion, or an offer to participate in any financial product, instrument, or program.

Any mention of SBLC, BG, MTN, PPP, monetization, structured finance, or trade finance

is purely illustrative and intended to promote understanding of global financing

mechanisms.

All real transactions require independent legal, tax, and regulatory assessments

by qualified professionals.

The objective of these publications is to contribute to global development by

promoting transparency, education, access to funding knowledge, and sustainable

solutions for social welfare, healthcare, housing, and humanitarian progress.

Contact

For confidential professional inquiries:

Email: info@nnrvtradepartners.com