⛽ Top 15 Oil Producers: 2000 vs 2025 The Strategic Energy Shift That Defines a Generation

This comprehensive 2000-word analysis breaks down how the global oil landscape changed dramatically between 2000 and 2025 — with hard data, trend interpretations, and geopolitical insight for professionals across energy, finance, and strategy.

🔍 The Oil Market at the Turn of the Millennium (2000)

In the year 2000, the global oil industry was dominated by large Western supermajors such as ExxonMobil, Shell, and BP — companies that were household names and symbols of energy capitalism. National Oil Companies (NOCs) were influential in their home regions but had not yet expanded into the global league of production dominance.

Back then, oil was a commodity largely shaped by corporate exploration, reserve competition, and private investment dynamics. The market was relatively decentralized — a patchwork of private giants and state producers.

• The Role of Western Majors

ExxonMobil produced approximately 2.5 million barrels per day in 2000. Shell was ahead at 2.3 million barrels per day, BP was visible, and TotalEnergies maintained around 1.5 mb/d.

Private ownership meant market decisions were influenced by shareholder expectations, quarterly reports, and capital efficiency. This era reflected what many analysts call the “Oil Corporate Age.”

📊 The Rising Force — National Oil Companies (NOCs)

By contrast, state-owned producers like Saudi Aramco and the National Iranian Oil Company were mostly confined to national output — with international partnerships but limited global commercial strategy beyond crude sales.

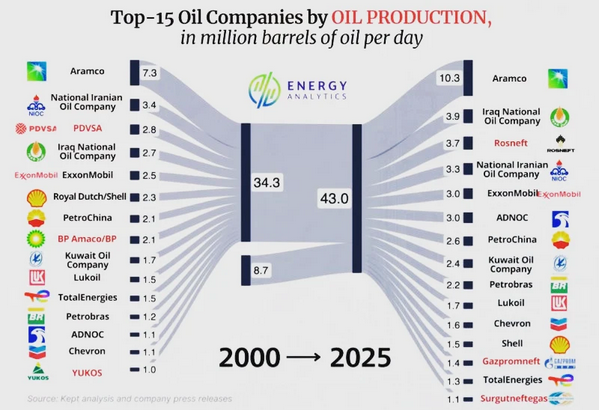

The production picture in 2000 looked like this:

| Company | Production (millions b/d) |

|---|---|

| Aramco | 7.3 |

| National Iranian Oil Company | 3.4 |

| ExxonMobil | 2.5 |

| Shell | 2.3 |

| TotalEnergies | 1.5 |

| Petrobras | 1.2 |

| ADNOC | 1.1 |

| Chevron | 1.1 |

| Other NOCs & Companies | ~13.3 |

Total global oil production was roughly 34.3 million barrels per day in 2000 — a figure that has since grown significantly.

📈 How the World Shifted by 2025

Fast forward to 2025, and the global oil map looks strikingly different. State producers have seized the lead across almost every metric of significance.

The latest production figures reveal:

| Company | Production (millions b/d) |

|---|---|

| Aramco | 10.3 |

| Iraq National Oil Co. | 3.9 |

| Rosneft | 3.7 |

| National Iranian Oil Company | 3.3 |

| ExxonMobil | 3.0 |

| ADNOC | 3.0 |

| PetroChina | 2.6 |

| Kuwait Oil Co. | 2.4 |

| Petrobras | 2.2 |

| Lukoil | 1.7 |

| Chevron | 1.6 |

| Shell | 1.5 |

| Gazpromneft | 1.4 |

| TotalEnergies | 1.3 |

| Surgutneftegas | 1.1 |

Total global production has expanded to approximately 43.0 million barrels per day by 2025 — reflecting both increased energy demand and strategic state investment.

📌 Trend #1 — NOCs Now Dominate the Energy Landscape

What was once a private-sector led industry is now overwhelmingly state-dominated. Saudi Aramco and ADNOC have expanded aggressively, benefiting from low lifting costs, integrated refineries, massive reserves, and sovereign strategies that prioritize long-term planning over quarterly earnings.

By 2025:

- Aramco produces more oil than any other company in history

- ADNOC tripled its production

- National Oil Companies now occupy the majority of the top 15 positions

📌 Trend #2 — Western Majors Shift Priorities

Meanwhile, traditional Western producers like Shell and TotalEnergies have reduced their upstream footprint. Many of these companies are reallocating capital toward renewables, divesting high-emission assets, or returning cash to shareholders via dividends and buybacks.

This shift reflects:

- ESG pressures from investors

- Regulatory constraints

- A strategic pivot to lower-carbon economies

- Market discipline over growth at all costs

🌍 Geopolitical Dimension of the Shift

This transformation isn’t just industrial — it’s geopolitical. State producers aren’t simply maximizing production; they are intentionally shaping energy policy, pricing power, and global influence.

Oil has become an instrument of national strategy — not just a traded commodity.

Saudi Arabia and the UAE leverage energy policy to influence OPEC+, coordinate with Russia, and manage global price stability. Iraq’s resurgence reflects renewed investment and infrastructure expansion. Russia’s Rosneft and Gazpromneft grew despite sanctions — showing how state backing can offset market limitations.

📊 Regional Shakeups and Production Hubs

Different regions have evolved in distinct ways:

- Middle East: Continued dominance, low operating costs, strategic expansion

- Russia & CIS: State consolidation and resilient production

- Asia: PetroChina and regional players grow modestly

- Americas: Petrobras expands via deepwater fields

- Europe: Western majors reduce upstream exposure

💼 What It Means for Businesses & Markets

For commodity traders, analysts, and energy strategists, this shift changes how you model risk and price fundamentals:

- Supply risk is more geopolitical

- Corporate performance is less tied to production growth

- Sanctions and national policy shape flows

- State actors coordinate supply via OPEC+ frameworks

- Price discovery becomes more opaque and political

📈 Long-Term Outlook

Looking ahead to 2030 and beyond:

- NOCs will remain entrenched

- Energy security becomes a strategic priority

- Investment in upstream will reflect national agendas

- Western majors will continue diversifying

- Renewables and LNG intersect with oil policy

📌 Key Takeaways

Strong shifts from private west-centric dominance toward state-driven global leadership are reshaping oil forever — and professionals must adapt.

📌 About the Author

Tiden — Trade Finance & Petroleum Markets Specialist

Expert in bank guarantees, inspection protocols, fuel markets, and energy logistics.

📧 Contact: info@nnrvtradepartners.com

⚠️ Disclaimer

Educational content only — not financial or operational advice.

About the Author

With extensive experience in international finance, the author structures high-level funding

solutions for governments, private corporations, public–private partnerships (PPP),

and large-scale development projects across energy, infrastructure, real estate,

education, healthcare, agriculture, and humanitarian sectors.

Operating through a global network of top-tier banks, institutional partners,

private capital groups, and regulated financial platforms, the author manages

confidential and compliant strategies involving SBLC, BG, MTN, DLC,

trade finance, structured finance, and monetization frameworks.

All processes follow strict AML/KYC, due diligence, and international regulatory

standards.

The author’s mission is to simplify access to world-class financial knowledge and

bring clarity to complex funding mechanisms, empowering governments, communities,

and project owners to realize transformative initiatives that enhance education,

healthcare, housing, clean energy, and economic development in emerging regions.

Professional Engagement & Confidentiality

All interactions are confidential, conducted with integrity, and aligned with

international compliance protocols.

No public fundraising, investments, or financial solicitations are offered.

Each project is treated with discretion, professionalism, and strategic precision.

Important Legal Disclaimer

This content is strictly educational and informational.

It does not constitute financial advice, investment solicitation, securities

promotion, or an offer to participate in any financial product, instrument, or program.

Any mention of SBLC, BG, MTN, PPP, monetization, structured finance, or trade finance

is purely illustrative and intended to promote understanding of global financing

mechanisms.

All real transactions require independent legal, tax, and regulatory assessments

by qualified professionals.

The objective of these publications is to contribute to global development by

promoting transparency, education, access to funding knowledge, and sustainable

solutions for social welfare, healthcare, housing, and humanitarian progress.

Contact

For confidential professional inquiries:

Email: info@nnrvtradepartners.com