Introduction — Why Most Buyers Fail to Prove Funds (And Lose Access to Real Sellers)

In EN590, Jet A1, and SBLC-backed petroleum transactions, the #1 reason real sellers reject buyers is simple:

The buyer cannot provide a clean, verifiable, institutional Proof of Funds (POF).

Most buyers send:

Screenshots from online banking

Edited PDFs

“Balance certificates” made in Excel

Outdated bank statements

Underfunded accounts

Non-verifiable comfort letters

These instantly disqualify them.

Real sellers, refiners, and title holders require institutional POF instruments issued through the banking system—never through email.

This article explains:

The 4 institutional POF instruments (RWA, BCL, MT799, Soft Bank Comfort Letter)

How each one works

Their legal and compliance value

When to use each

Which instruments sellers accept

Which instruments NNRV recommends

The exact banking workflow

The biggest risks buyers face when proving funds

A comparison table used at refinery level

This is the 2025 definitive guide.

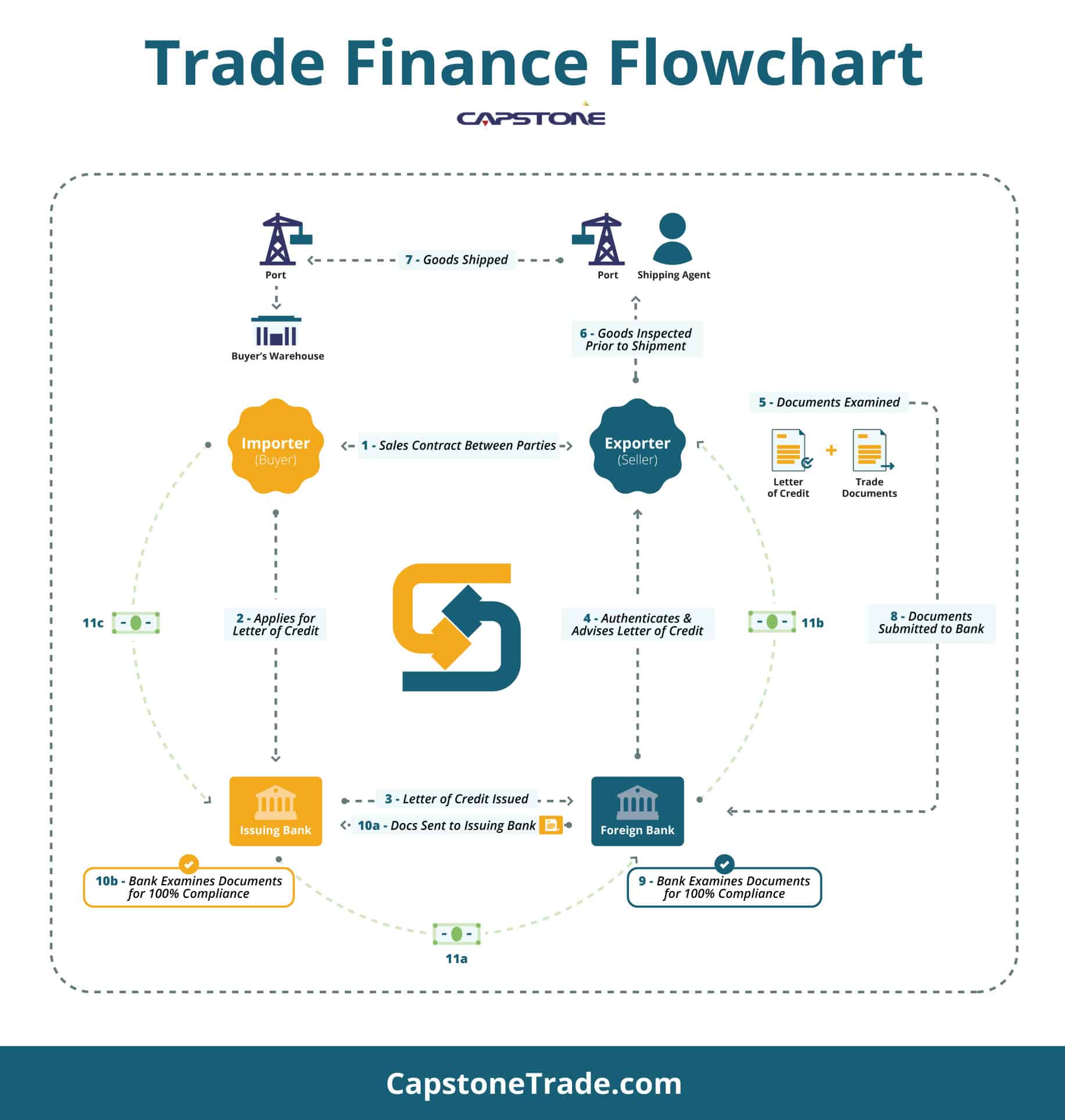

SECTION 1 — Understanding the Context: Why POF Is Mandatory (Macro + Industry)

1.1 Why Sellers Require Proof of Funds Before POP or SPA Execution

Real sellers and terminals operate under strict compliance laws:

AML (Anti-Money Laundering)

CFT (Counter-Terrorist Financing)

Basel III

OFAC / EU Sanctions

Trade finance risk mitigation

Tank and vessel scheduling rules

Before releasing:

Tank numbers

TSR

ATV/CPA

SPA

Full POP

DTA

DIP test authorization

…the seller MUST confirm the buyer is financially capable.

POF is not about trust.

POF is about compliance and risk control.

1.2 Fake Buyers Flood the Market

In 2025, the petroleum market is flooded by:

Brokers pretending to be buyers

Buyers with no financial backing

Traders without bank instruments

Investors seeking “no upfront” deals

People claiming RWA without bank support

Because of this, real sellers filter 90% of buyers using POF.

1.3 Institutions Require Bank-to-Bank Verification

A real POF must always be:

✔ Issued by a bank

✔ Verifiable through SWIFT

✔ Linked to a real account

✔ Signed by bank compliance

✔ Sent only bank-to-bank

Anything else is invalid.

SECTION 2 — The 4 Real Instruments for Proving Funds (A to Z Explanation)

Below are the only 4 legitimate forms of POF recognized by sellers, refineries, and terminals.

1. RWA — Ready, Willing & Able Letter

✔ Definition

A formal statement from the buyer’s bank confirming they are:

Ready to engage

Willing to proceed

Able to pay or issue bank instruments

✔ Use Case

TTT/FOB/CIF petroleum deals

SBLC/LC issuance

Monetization operations

High-value commodity deals

✔ What It Proves

Buyer’s intent

Bank relationship

Financial standing

✔ Limitations

Does not prove exact balance

Not binding

Not a payment guarantee

2. BCL — Bank Comfort Letter

✔ Definition

A bank letter confirming:

The buyer’s account status

The buyer’s financial capacity

The buyer’s reputation and credit relationship

✔ Use Case

Commodity trades

Soft proof for mid-cap deals

Pre-SPA confidence check

✔ What It Proves

That the buyer holds funds

That the bank is comfortable supporting the transaction

✔ Limitations

Not a guarantee

Cannot substitute MT799 or MT103

Some sellers reject BCL due to fraud risks

3. MT799 — SWIFT Proof of Funds (Preadvice)

✔ Definition

A SWIFT MT799 is a bank-to-bank message confirming:

Availability of funds

Intent to engage

Readiness to block/issue instruments

Compliance clearance

This is the gold standard for POF.

✔ Use Case

EN590/Jet A1 TTT

FOB loading

CIF + LC transactions

SBLC monetization

Supplier verification

✔ What It Proves

Real funds

Real account

Real banking capacity

KYC cleared

✔ Limitations

Requires buyer to have institutional bank

Cannot be sent by small banks or fintechs

Requires compliance approval

Not suitable for unprepared buyers

4. Bank Comfort / Soft POF Letter (Non-SWIFT)

✔ Definition

A simple bank letter (email or PDF) confirming:

Account ownership

Account balance (optionally)

Basic creditworthiness

✔ Use Case

Early pre-qualification

DIP test pre-negotiations

Low-risk trades

✔ Limitations

Weakest form of POF

Not bank-to-bank

Not SWIFT-verifiable

Fraud-prone

Rejected by 80% of real sellers

SECTION 3 — NNRV Expert Analysis: Which POF Is Best?

POF Requirements Vary by Delivery Mode

| Delivery | Minimal POF | Institutional POF |

|---|---|---|

| TTT Rotterdam | RWA or BCL | MT799 |

| FOB | RWA | MT799 |

| CIF LC | BCL | LC via MT700 |

| SBLC Monetization | RWA | MT799 → MT760 |

| Large Off-Takes | RWA + CPA | MT799 + MT103 |

Top Buyer Mistakes (NNRV Perspective)

Sending PDF bank statements

Sending screenshots

Sending personal bank accounts

Using fintech banks with no SWIFT capability

Refusing to send bank-to-bank communication

Expecting POP before POF

Using fake or outdated RWA/BCL

Top Seller Mistakes

Requiring MT799 too early

Not offering soft procedures for real buyers

Rejecting legitimate BCLs prematurely

Not coordinating buyer’s bank with terminal schedule

Allowing brokers to interfere in POF flow

Real Seller Expectations (Institutional)

A real seller accepts:

RWA for pre-qualification,

BCL for early comfort,

MT799 after SPA,

MT103 for payment,

MT760 for SBLC-backed deals.

Anyone asking for:

MT799 before SPA

MT103 before DIP

Full POP before POF

CPA before ICPO

…is fake or inexperienced.

SECTION 4 — Step-by-Step POF Process Before SPA & POP

STEP 1 — Buyer Submits ICPO + Corporate KYC (Day 1–2)

Includes buyer procedure acceptance.

STEP 2 — Seller Pre-Screens Buyer (Day 2–3)

Verifies legitimacy.

STEP 3 — Soft POF (RWA or BCL) (Day 2–5)

Required before any POP release (partial).

STEP 4 — SPA Issued (Day 5–10)

Seller issues SPA after confirming credibility.

STEP 5 — Bank-to-Bank MT799 (Day 7–14)

Triggers POP, DTA, or vessel nomination.

STEP 6 — DIP Test or Loading Protocol (Day 10–20)

Inspection begins.

STEP 7 — MT103 Payment (Day 12–22)

Final payment and title transfer.

SECTION 5 — Buyer & Seller Questions (20 Total)

10 Buyer Questions

Does MT799 show my exact balance? (No.)

Is BCL enough for real sellers? (Often for pre-qualification.)

Do I need MT799 for TTT? (Yes, 90% of the time.)

Can I avoid SWIFT? (No, not for institutional deals.)

Does RWA expose my bank info? (Only to seller’s bank.)

Can a fintech bank send MT799? (No.)

Do sellers accept escrow accounts? (Rare.)

Can I do DIP test without POF? (Never.)

Can I use an SBLC as POF? (Yes, if valid.)

Can NNRV validate my POF? (Yes.)

10 Seller Questions

Should I accept screenshots? (No.)

Which POF confirms a real buyer? (MT799.)

Should POF be before SPA? (Soft POF yes, MT799 no.)

What if buyer refuses bank-to-bank? (Reject.)

Can brokers handle POF? (Never.)

Should I show POP before POF? (No.)

When do I issue DTA? (After SPA + MT799.)

Should I share tank numbers before MT799? (No.)

Can I ask for MT103 before DIP? (Impossible.)

How to avoid fake buyers? (NNRV pre-screening.)

SECTION 6 — Institutional Proof & Credibility

The POF structures described reflect the protocols of:

HSBC

Barclays

BNP Paribas

Deutsche Bank

Standard Chartered

UOB / OCBC / DBS

Citibank

Corresponding compliance frameworks:

✔ Basel III liquidity rules

✔ FATF AML

✔ OFAC/EU Sanctions

✔ SWIFT messaging standards

✔ Port authority rules

This is the global standard for petroleum transactions and SBLC-backed trades.

SECTION 7 — Professional Call to Action (CTA)

📌 Need to Prove Funds Safely & Professionally?

NNRV Trade Partners can structure your RWA, BCL, MT799, or SBLC workflow from A–Z.

We provide:

POF review

Bank instrument verification

RWA/BCL drafting

MT799 coordination

SPA alignment

Full seller-side acceptance guidance

Institutional buyer/seller onboarding

📩 info@nnrvtradepartners.com

🌐 www.nnrvtradepartners.com

Mini FAQ (5 Key Questions)

Can NNRV check my RWA or BCL for authenticity?

Yes — instantly.Do all sellers accept BCL?

No — depends on risk level.Is MT799 mandatory for TTT?

Usually yes.Can DIP test happen with only RWA?

Not in 2025.Can fintech banks issue RWA/MT799?

No — SWIFT capability required.

Why Choose NNRV Trade Partners?

Institutional compliance

Real refinery and seller access

Expertise in SBLC/LC, MT799, MT760, RWA

Full POF structuring

Zero-fraud filtration

Bank-to-bank coordination

Global buyer & seller onboarding

Confidential and professional