Price Evolution of Marine Fuel Oils and Brent Crude Oil

The price evolution of intermediate fuel oil, marine diesel oil (MDO) and marine gas oil (MGO) in Rotterdam — compared with Brent crude oil — reveals important trends in the bunker fuel market. Bunker fuels such as IFO 380 (heavy fuel oil), MDO and MGO are key operating costs for global shipping, and their pricing dynamics are influenced by crude oil prices, refinery yields, environmental regulations, and logistical factors. :contentReference[oaicite:2]{index=2}

Heavy fuel oil (HFO) like IFO 380 has historically been priced relative to crude benchmarks such as Brent, which remains one of the dominant reference prices for global oil markets. Brent crude’s price sets the tone for many refined products and residual fuels used in maritime and industrial applications. :contentReference[oaicite:3]{index=3}

Understanding the Price Trends

The graph above shows how the prices of IFO 380, MDO and MGO moved alongside Brent crude prices over multiple years. These fuel prices fluctuate based on several key drivers:

- Crude oil price movement: As Brent crude moves up or down, fuel oil prices tend to follow, though refined products like MGO often trade at a premium due to processing costs and regulatory demands. :contentReference[oaicite:4]{index=4}

- Refinery outputs: The yields of heavy versus light distillates affect relative pricing. Increased refining of light crude decreases heavy fuel yields, potentially lifting IFO prices.

- Environmental regulations: Sulphur emissions controls (e.g., IMO 2020) shift consumption from heavy fuel oil toward cleaner distillates like MDO and MGO.

- Shipping demand cycles: Periods of strong global trade increase bunker fuel demand, affecting price spreads.

Key Observations from the Evolution Graph

• **Heavy fuel oil (IFO 380)** generally trades below lighter distillates, but can spike significantly when crude prices surge. • **Marine diesel oil (MDO)** and **marine gas oil (MGO)** often trade at higher prices, reflecting the cost of refining and lower sulphur content. • Price spreads widen when crude markets are volatile, such as during economic shocks or transitions to low-sulphur fuels. :contentReference[oaicite:5]{index=5}

This evolution is critical for ship operators, as bunker fuel represents a large portion of vessel operating costs. Understanding the correlation between crude benchmarks and bunker prices enables better bunker procurement strategies and cost forecasting.

Why Brent Matters

Brent crude oil is a major benchmark for global oil pricing and is widely used in the Atlantic basin. Changes in Brent prices ripple through refined product markets, including marine fuels and other distillates. As a result, movements in Brent are closely watched by shipowners, traders, and refiners alike. :contentReference[oaicite:6]{index=6}

What This Means for the Shipping Industry

The relative price movements among IFO 380, MDO and MGO have practical business implications:

- Cost planning: Predicting bunker bill impacts as crude markets shift.

- Fuel switching: Deciding between residual fuels and distillates based on cost and emissions compliance.

- Sustainability compliance: Evaluating the economic impact of environmental regulations on fuel choices.

As the industry transitions toward cleaner fuels, understanding these price relationships becomes crucial for effective procurement and fleet deployment strategies.

Price Evolution of Marine Fuels vs Brent Crude: How The Low-Sulphur Transition Reshaped Shipping Economics

Source: Own compilation based on Clarkson data — adapted from Notteboom (2011)

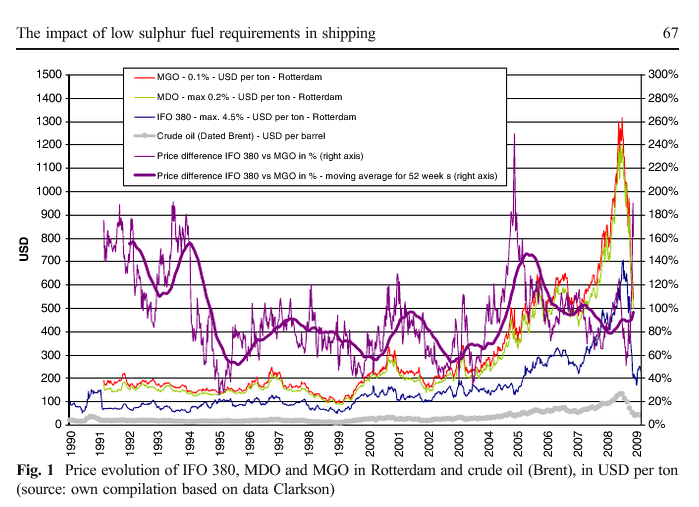

Over the past two decades, the marine fuel market has undergone a dramatic transformation. A combination of stricter environmental regulations, volatile crude oil prices and the emergence of cleaner distillate fuels reshaped the cost structure of global shipping. The graph above illustrates the long-term price evolution of IFO 380 (bunker fuel), MDO (marine diesel oil), MGO (marine gasoil) and Brent crude oil in USD per ton.

While the relationship between marine fuels and crude oil historically followed a predictable pattern, policy-driven disruptions — particularly sulphur reduction mandates — fundamentally altered how fuel spreads behave. For shipowners, cargo operators and logistics planners, understanding these dynamics is now essential to maintaining competitiveness.

1. From Heavy Fuel Oil Dominance to a Multi-Fuel Market

Before 2010, global shipping relied overwhelmingly on IFO 380, a high-sulphur residual fuel produced from the bottom of the refining barrel. Its price closely mirrored crude oil but at a significant discount due to its lower quality and limited applicability outside the maritime sector.

The introduction of Emission Control Areas (ECAs) in Northern Europe and North America changed this dynamic. Ships entering these zones were required to burn distillate fuels such as MGO or MDO, pushing demand toward more refined products with higher production costs.

This regulatory split created a dual market: cheap heavy fuels for open oceans and much more expensive low-sulphur distillates for ECAs.

Price spread widens

As the chart indicates, the period from 2008 to 2015 marked a sustained widening of the spread between IFO 380 and MGO. This spread became a central factor influencing vessel deployment, fuel purchasing strategies and investment in exhaust gas cleaning systems.

2. The 2015–2020 Shift: Tightening Regulations and New Cost Structures

The global maritime sector faced unprecedented regulatory tightening during this period. IMO 2020 — the mandate limiting sulphur content in marine fuel to 0.5% globally — was the most impactful policy development in the history of bunker fuel markets.

In anticipation of IMO 2020, refineries ramped up production of low-sulphur alternatives, including Very Low Sulphur Fuel Oil (VLSFO). While not shown in the historical chart above, the pre-transition period caused distortions in the prices of MGO, MDO and Brent.

Distillate markets strengthened as refiners redirected capacity from high-sulphur fuel oil toward diesel-like products. As a result, MGO prices decoupled from Brent and began behaving increasingly like traditional road diesel.

3. Competitiveness of RoRo Shipping in Northern Europe

Northern Europe’s RoRo segment was among the most affected by low-sulphur requirements. Unlike long-haul container vessels, RoRo ships operate on short, frequent routes — often spending a significant share of their voyage time inside ECAs.

This meant a persistent cost penalty for operators unable to switch fuels or retrofit scrubbers. Fuel now represents up to 60% of voyage costs on certain RoRo routes, making fuel strategy a defining factor of market competitiveness.

Operators faced three options:

- Switch fully to distillate fuels (MGO/MDO)

- Adopt VLSFO blends after 2020

- Install scrubbers and continue burning IFO 380

Each option offered a different cost-risk profile depending on crude oil volatility, refining spreads and capital availability.

4. Understanding the Price Behavior of Marine Fuels

The evolution shown in the chart demonstrates several key principles:

A. Heavy fuel oil tracks crude but with increasing volatility

Structural decline in residual fuel demand — driven by environmental regulation — gradually reduced the stability of IFO 380 pricing. As fewer refineries prioritized heavy fuel production, supply became more sensitive to operational disruptions.

B. Distillate fuels increasingly reflect diesel market fundamentals

MGO and MDO prices now behave like ultra-low-sulphur diesel, affected by:

- Seasonal heating demand

- Road transport consumption

- Refinery maintenance cycles

- Geopolitical shocks impacting middle distillates

C. The spread became a strategic variable

For shipowners, the economic decision between installing scrubbers or consuming MGO was entirely dependent on the expected IFO–MGO spread. When spreads exceed USD 250 per ton, scrubbers become highly attractive. When spreads collapse, distillates regain competitiveness.

5. Looking Ahead: New Marine Fuel Paradigms

As the energy transition accelerates, shipping fuel markets will continue to shift. LNG, methanol, ammonia and biofuels introduce new cost curves that interact with traditional fuels. However, for the foreseeable future, diesel-like fuels will remain dominant, particularly in RoRo, short-sea shipping and high-frequency liner services.

The historical price evolution shown in the chart serves as a reminder: **regulation, not geology, now determines the economics of marine fuels**.

Conclusion

The transition from high-sulphur to low-sulphur marine fuels did more than reshape compliance strategies — it fundamentally altered the cost structure of global shipping. By comparing IFO 380, MGO, MDO and Brent crude price trends, it becomes clear that environmental regulation has permanently redefined fuel economics.

For operators in competitive segments such as Northern European RoRo, fuel strategy is no longer an operational detail — it is a decisive commercial advantage. Understanding fuel price behavior, spreads and long-term trends is now essential for maintaining profitability.

Source: Notteboom, T. (Adapted). “Price evolution of IFO 380, MDO and MGO in Rotterdam and Brent crude oil.” Based on Clarkson Research data.

About the Author

This article was prepared by NNRV Trade Partners as part of its ongoing research and insights into global fuel markets, shipping economics and trade finance. For inquiries, collaborations or media use:

Email: info@nnrvtradepartners.com

Disclaimer: This content is provided for informational and educational purposes only. It does not constitute financial, legal or investment advice.

About the Author

With extensive experience in international finance, the author structures high-level funding

solutions for governments, private corporations, public–private partnerships (PPP),

and large-scale development projects across energy, infrastructure, real estate,

education, healthcare, agriculture, and humanitarian sectors.

Operating through a global network of top-tier banks, institutional partners,

private capital groups, and regulated financial platforms, the author manages

confidential and compliant strategies involving SBLC, BG, MTN, DLC,

trade finance, structured finance, and monetization frameworks.

All processes follow strict AML/KYC, due diligence, and international regulatory

standards.

The author’s mission is to simplify access to world-class financial knowledge and

bring clarity to complex funding mechanisms, empowering governments, communities,

and project owners to realize transformative initiatives that enhance education,

healthcare, housing, clean energy, and economic development in emerging regions.

Professional Engagement & Confidentiality

All interactions are confidential, conducted with integrity, and aligned with

international compliance protocols.

No public fundraising, investments, or financial solicitations are offered.

Each project is treated with discretion, professionalism, and strategic precision.

Important Legal Disclaimer

This content is strictly educational and informational.

It does not constitute financial advice, investment solicitation, securities

promotion, or an offer to participate in any financial product, instrument, or program.

Any mention of SBLC, BG, MTN, PPP, monetization, structured finance, or trade finance

is purely illustrative and intended to promote understanding of global financing

mechanisms.

All real transactions require independent legal, tax, and regulatory assessments

by qualified professionals.

The objective of these publications is to contribute to global development by

promoting transparency, education, access to funding knowledge, and sustainable

solutions for social welfare, healthcare, housing, and humanitarian progress.

Contact

For confidential professional inquiries:

Email: info@nnrvtradepartners.com